Two identical firms. One is three times as profitable. Why?

Picture two law firms.

They are the same size. They have the same number of partners and employ the same number of lawyers beneath them, drawn from the same law schools and trained to the same standard. They operate in the same cities. They serve the same kinds of clients — Fortune 500 companies and financial institutions — and the same household names appear on both client lists. They do the same kind of work, at the same level of technical excellence. If you sat in on their pitches, read their advice, and met their people, you would struggle to tell them apart.

One of them is two to three times as profitable as the other.

Not ten per cent. Not thirty. Two to three times — measured in overall profitability or profit per partner, the numbers these firms care about most. Year after year. Consistently enough that it cannot be an accident of one good year or one large matter.

The question is simple, and most partners have never seriously asked it: what could possibly account for that difference?

“One of them is two to three times as profitable as the other. Not ten per cent. Not thirty. Two to three times.”

Ruling out the easy answers

In most industries, you could explain a profit gap of that size without much difficulty. One company owns critical intellectual property the others cannot touch — a pharmaceutical patent, a piece of proprietary technology. One operates behind a regulatory barrier that keeps competitors out. One controls a physical asset, a network, a piece of infrastructure that nobody else can replicate. One enjoys the kind of scale that produces a near-monopoly.

None of this applies in the premium legal market.

There is no patent on legal expertise. There is no regulatory moat protecting one elite firm from another. There are no physical assets that bar entry. There is no Big Four equivalent dominating the top tier — even the firms in the lower half of the rankings are substantial, well-known names doing serious work for serious clients. Barriers to entry and exit are low. Clients are sophisticated and price aware. They constantly re-evaluate their choices and move when they have reason to.

This is about as close to a pure, frictionless market as exists anywhere in professional services. Which is precisely what makes it so revealing. When you strip away IP, regulation, assets, and monopoly, the usual explanations for a profit gap disappear. And yet the gap remains — large, consistent, and unmistakable.

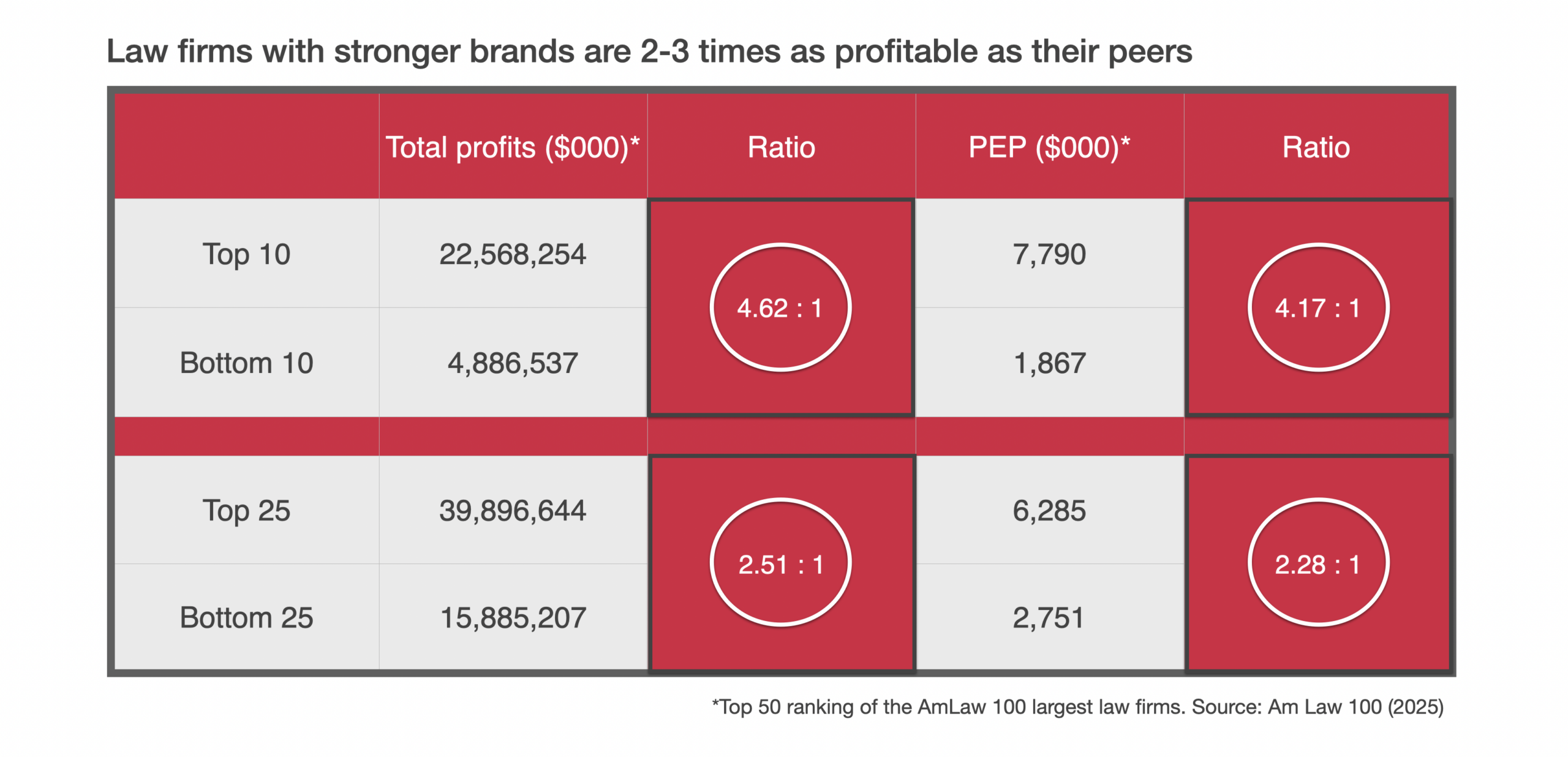

And it is not a matter of a single fortunate pair. The legal industry publishes its own performance data every year, and the pattern holds across the entire population of top firms. Compare the top ten firms with the bottom ten of the top fifty, and the profitability difference runs to around four times. Compare the top twenty-five with the bottom twenty-five, and it is still more than double. These are not outliers set against stragglers. They are near-identical institutions, and the gap between them is systematic.

So what is left?

So what is left?

The thing we have been walking past

Here is where most intelligent professionals hesitate. Because the answer, when you arrive at it, is the one thing they have spent their careers quietly dismissing.

The difference is brand.

And the moment that word appears, something predictable happens. A mental image surfaces — a logo, a colour palette, a website, a brochure. The reflex is immediate and almost universal: brand means visual identity, visual identity is marketing decoration, and marketing decoration is not what drives the profitability of a serious professional firm. The word has been filed, long ago and without much thought, under “fluff.”

That reflex — brand means logo, logo means fluff — is what keeps firms from ever examining the gap they have just seen.

Because the brand that explains the profit gap has almost nothing to do with logos. It is something far more consequential: the sum of everything the market believes about a firm before it has done a day’s work on the matter at hand. It is what a firm is understood to stand for. It is what it is known to be best at. It is the reason one firm gets the call for the most significant, most sensitive, most lucrative work — and another, equally capable firm, does not.

That is brand in its true sense. Not what a firm looks like. What the market believes about it. And in a frictionless market, where clients can choose anyone and competence is assumed, what the market believes is very nearly the only thing that determines who wins the best work at the best rates.

“Excellence and brand are not rivals. They are the same thing, seen from two sides. The only difference between them is the word ‘perceived.'”

But isn’t it all about excellence?

There is a second objection, and it is more thoughtful than the first. It does not reach for the logo. It says something like this: we don’t need to worry about brand, because we focus on being excellent — and excellence is what the market rewards.

This deserves to be taken seriously because it comes from the right place. It reflects the organising belief of almost every professional career: that you are selected, trained, promoted, and rewarded on the quality of your work. Excellence is the currency. To suggest that something as soft-sounding as brand could matter as much as technical mastery can feel almost like an affront to that belief.

But the objection contains a hidden assumption that does not survive examination. It assumes that the market rewards excellence. It does not. The market rewards perceived excellence — and the gap between those two things is the whole of the argument.

Actual excellence is what happens in the room: the quality of the thinking, the judgment, the work itself. Perceived excellence is what the market believes about that quality — and most of the people forming that belief have never been in the room and never will be. A client choosing between two elite firms cannot audit the underlying legal reasoning before they instruct. However sophisticated they are, they are buying something they cannot fully verify in advance. So, they choose on what they perceive. And the firms that are genuinely excellent but not perceived to be so are the ones that quietly struggle.

This is why the patrician adviser of an earlier era — brilliant, dismissive of client experience, certain that expertise alone would carry the day — is now a vanishing figure. Excellence the market cannot perceive, trust, and easily choose is excellence that goes unrewarded.

So the excellence partner is not wrong. They have simply not noticed that they have already conceded the argument. They believe excellence drives reward — and it does, but only once it has been perceived. And perceived excellence, made legible and credible to a market that cannot directly verify it, is precisely what brand, in its true sense, is.

Excellence and brand are not rivals. They are the same thing, seen from two sides. The only difference between them is the word “perceived” — and that word is worth, as the data shows, two to three times the profit.

“They are not there because their lawyers are two to three times better than everyone else’s. They are there because the market believes something about them that it does not believe about their peers.”

Why belief is worth so much

Consider how the most valuable work actually gets awarded.

A general counsel facing a bet-the-company dispute, or a board contemplating its most consequential transaction, is not buying billable hours. They are buying confidence. They need to choose an adviser they can trust with the outcome, justify that choice to colleagues and stakeholders, and defend the premium fee that choice involves. In that moment, the firm’s reputation is doing the heavy lifting — before a single piece of advice has been given.

The firm the market believes in commands more of the work that matters, wins more of it when it competes, and charges more for it when it does. Reputation drives which opportunities arrive. Perceived distinctiveness drives which of those opportunities convert. And the confidence a firm’s name inspires drives what it can charge. Each of these compounds on the others. I have set out the mechanism by which brand perception converts into profit at each of these stages in more detail elsewhere (see further reading below).

That is not decoration. That is the engine of the firm’s profitability — and it is precisely what the word “brand” actually describes, once you set aside the logo.

Beyond law

It is worth being clear that this is not a quirk of the legal profession. Law simply happens to provide the cleanest evidence, because its performance data is public, detailed, and submitted annually by the firms themselves. That transparency makes it a natural experiment that other sectors cannot match.

But the underlying mechanism is not specific to law. It applies wherever firms compete in a market without the artificial advantages that distort profitability elsewhere — proprietary IP, regulatory protection, controlled assets, monopoly scale. Consulting, accountancy, architecture, engineering, advisory, agency work: in any premium professional services market where competence is assumed, clients are sophisticated, and the real differentiator is what the market believes, the same logic holds. The numbers are harder to see outside law, because the data is private. The dynamic is exactly the same.

The question worth sitting with

The two to three times profit difference is not a marketing statistic. It is published, every year, in data the legal industry trusts and submits to itself. It describes firms that are, on every measurable dimension, near-identical to one another. The only material variable left to explain it is the one most firms have never seriously examined.

This does not mean a firm can simply decide to be more profitable. Reputation is hard-won and cannot be conjured. That is a genuine challenge, and a separate conversation. But it is a conversation no firm will ever have if it continues to file brand under fluff, glance past it, and return to discussing headcount and utilisation.

The firms at the top of those profitability rankings are not there by accident, and they are not there because their lawyers are two to three times better than everyone else’s. They are there because the market believes something about them that it does not believe about their peers — and that belief is worth an extraordinary amount of money.

So the question those two near-identical firms leave us with is not “how do we work harder?” It is “what does the market actually believe about us — and have we ever truly tried to shape it?”

Most firms have never asked it. That, more than anything, is the opportunity.

Further reading

If this has prompted you to reconsider what brand actually means for a professional services firm, three related pieces take the thinking further:

BIG B Brand vs little b brand — on the crucial distinction between brand as visual identity and brand as strategic reputation.

The Hidden Gem Problem — on the firm that is genuinely excellent but under-perceived by the market.

The False Choice at the Heart of Most Positioning Conversations — on how a firm finds a position that is both distinctive and large enough to grow into.

And for a deeper dive into the specific mechanism by which brand perception drives profitability — through awareness, conversion, and pricing — see Brand: The Key to 50%+ Profitability.

If you enjoyed this article please like and share with others. If you want to recieve more like this from Principia you can subscribe here (bottom of page).

Subscribe to Espresso Branding

A regular shot of brand stimulation from Ian